S. Pittet, Rétrocessions : Pas d’obligation de restitution même en présence d’une relation de conseil ?, (10 juin 2026) <https://cdbf.ch/fr/1465/>

Articles en relation

Plus d'articles en relation

Retrocessions

No obligation to return retrocessions even where an advisory relationship exists ?

(Translated by DeepL)

In an investment advisory relationship, if the client carries out transactions that do not result from advice given by the bank, the bank is not in a position of conflict of interest and may retain the retrocessions received (ACJC/439/2026 of 10 March 2026, which has entered into force).

In 2015, an experienced and wealthy British client opened an investment advisory relationship with a bank domiciled in Geneva. According to the contractual documentation, the client had direct access to the trading room. The bank also undertook to provide him with advice, either on its own initiative or upon request. Over a two-year period, the bank provided advice on an ad hoc basis, which was not always followed by the client.

During the course of the relationship, the bank received retrocessions totalling CHF 41,886. This sum corresponds to eight retrocessions of 1 % received on the value of eight structured products purchased by the client in 2016 and 2017. Through a debt collection agency to which the client has assigned his claims, the bank is being ordered to repay this amount.

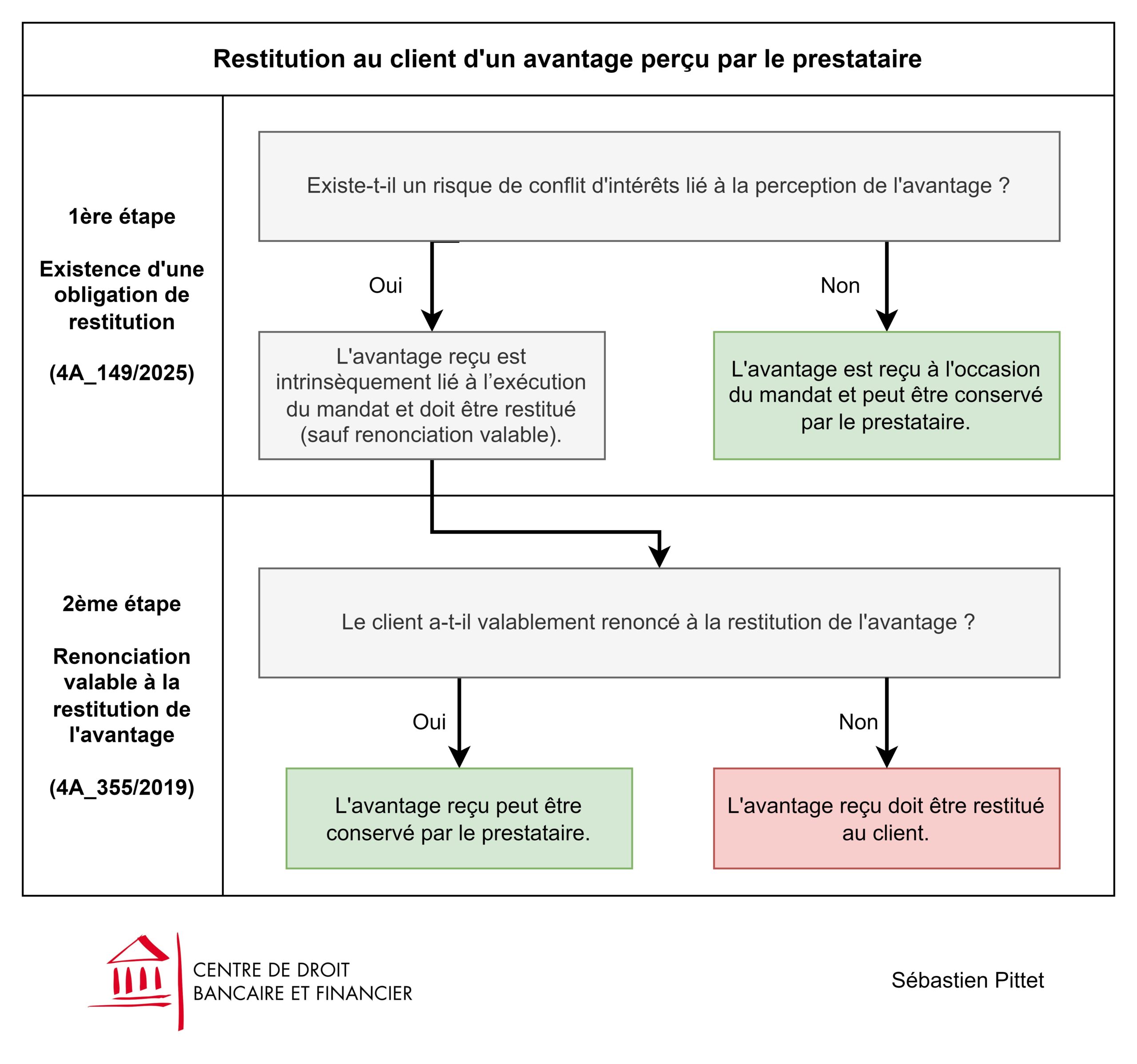

The issue of the repayment of retrocessions can be divided into two stages. Firstly, it must be analysed whether the benefit received by the agent is subject to an obligation to repay. If so, the second step is to determine whether the principal has validly waived the obligation to repay the retrocessions, as the obligation to repay is of a discretionary nature (see summary diagram). Over the past twenty years or so, case law has clarified the scope of the agent’s duty to inform, enabling the principal to waive the obligation to return the commissions (second stage ; see in particular 4A_355/2019, discussed in Fischer, cdbf.ch/1145/). Recently, in case law concerning execution only, the Federal Supreme Court has examined more closely the existence of an obligation to return (first stage, see 4A_149/2025, discussed in Liégeois, cdbf.ch/1453/). The judgment discussed here forms part of the analysis of this first stage of reasoning, namely the basis for the obligation to return.

{kind=link}

To determine whether the retrocessions must be returned in this case, the Court of Justice of the Canton of Geneva bases its reasoning on judgment 4A_149/2025. According to this case law, to determine whether a benefit received from a third party is intrinsically linked to the performance of the mandate and must be returned, it is necessary to analyse the existence of a risk of a conflict of interest. Where the agent may be tempted not to take sufficient account of the interests of his principal, the benefits received must be returned (unless there is a valid waiver). If this is not the case (no conflict of interest), the benefits may be retained.

Like the Federal Court, the Court of Justice points out that a conflict of interest may exist in the context of an investment advisory relationship. Indeed, the adviser may be tempted to recommend to their client the products that generate the highest remuneration for them. In the present case, however, it has not been shown that the investments giving rise to the disputed retrocessions were made on the basis of advice from the bank. The eight investments in structured products were therefore acquired on an ‘execution only’ basis. In the absence of any influence by the bank on the investment decision-making process, the risk of a conflict of interest is ruled out. It follows that the retrocessions do not have to be returned, as they are not intrinsically linked to the execution of the mandate.

This cantonal decision reinforces the case-by-case nature of the analysis of the obligation to return retrocessions. To determine whether a benefit must be returned to the client, a case-by-case analysis of the risk of a conflict of interest is necessary. The existence of an investment advisory relationship does not in itself allow one to conclude that a risk of a conflict of interest exists. The client must also provide evidence that the investments on which retrocessions were received were made on the bank’s advice.

Regardless of the issue of retrocessions, this decision also provides an opportunity for a more general observation on the various contracts governing a banking relationship. Case law frequently analyses wealth management, investment advisory and ‘execution only’ services in isolation. The reality is often more nuanced. As this judgment illustrates, these different services can coexist. Where the client has access to the trading floor, an ‘execution-only’ relationship exists, even in the absence of a formal contract (in reality, this often stems from the general terms and conditions signed by the client). One or more additional services – for example, advisory services – are then added to this basic relationship, and these in turn are the subject of specific contractual documentation.